Would you like to get the latest insights on real estate market trends and technology?

An Inside View on Real Estate Profit Margins

--

Earnings matter. This is as true in energy, industrials and consumer staples as it is in real estate. After all, people invest in real estate to make money, so keeping an eye on profit margins is a must. MPF Research thought it would be interesting to view real estate performance in term of net profit margins similar to the way corporate profitability is measured.

We define net profit margin as reported net income / rental revenue. More specifically, this analysis is based on publicly traded REITs with a minimum of $100 million in annual revenue and at least 10 years of operating performance. There were two exceptions: Monmouth Real Estate Investment Corporation, an industrial REIT which fell below the revenue threshold, and Douglas Emmett, Inc., an office REIT which went public in 2006, falling short of the time requirement. (A full list of component companies is provided at the end.)

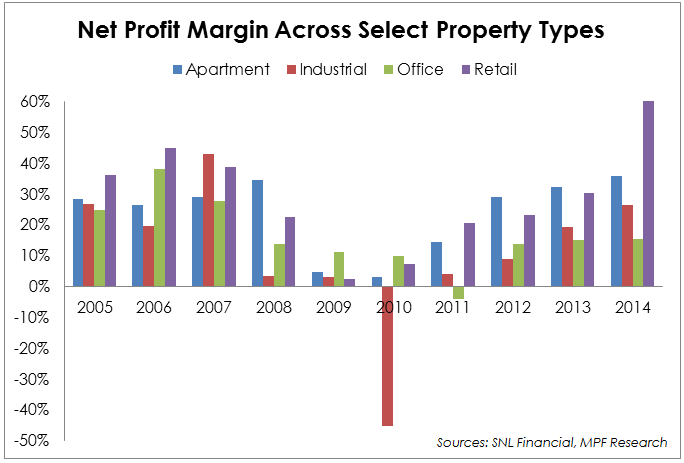

The findings are interesting. First, real estate is a profitable industry. Based on research by Dr. Ed Yardeni, the reported net profit margin for the S&P 500 was 7.7% in 2014. For comparison, all four major property types were well in excess, ranging from 15.2% in the office sector to 61.7% in retail during the same time period. Second, since reporting a disastrous 2010, industrial has shown incredible momentum as longer-term lease expirations are being marked to market. Third, in terms of net profit margins, retail and apartment performance stand out. Over the past 10 years of operating results, the average profit margin is as follows:

- Retail (28.7%)

- Apartment (23.7%)c

- Office (16.5%)

- Industrial (10.8%)

It is important to remember reported net income is subject to one-time events which can dramatically impact the results. For instance, in 2010, industrial performance was heavily impacted by ProLogis’s roughly $1.2 billion loss due principally to a write down of goodwill, impairment charges and loss on early extinguishment of debt, according to company filings. Conversely, one-time gains impact reported net income in the other direction. For example, in 2014, retail posted a staggering net profit margin. In this case, The Macerich Company benefited from a $1.4 billion remeasurement gain stemming from the acquisition of the 49% ownership interest that the company did not previously own in two separate joint ventures. And Taubman Centers recorded a $1.1 billion gain from the disposition of multiple assets.

Overall, using a 10-year average of net profit margin should reduce some of the noise and the output provides a new perspective across select property types. In the end, the real estate industry is cyclical, but the long-term health is welcome news to industry participants.

Component companies

Apartment: Apartment Investment and Management Company Associated Estates Realty Corporation, AvalonBay Communities, Inc., Camden Property Trust, Equity Residential, Essex Property Trust, Inc., Home Properties, Inc., Mid-America Apartment Communities, Inc., Post Properties, Inc., UDR, Inc.

Industrial: DCT Industrial Trust Inc., EastGroup Properties, Inc., First Industrial Realty Trust, Inc., Monmouth Real Estate Investment Corporation, Prologis, Inc.

Office: Alexandria Real Estate Equities, Inc., Boston Properties, Inc., Brandywine Realty Trust, Columbia Property Trust, Inc., Corporate Office Properties Trust, Cousins Properties Incorporated, Douglas Emmett, Inc., Equity Commonwealth, Highwoods Properties, Inc., Kilroy Realty Corporation, Mack-Cali Realty Corporation, Parkway Properties, Inc., Piedmont Office Realty Trust, Inc., SL Green Realty Corp.

Retail: DDR Corp., Federal Realty Investment Trust, General Growth Properties, Inc., Kimco Realty Corporation, Macerich Company, National Retail Properties, Inc., Realty Income Corporation, Regency Centers Corporation, Simon Property Group, Inc., Taubman Centers, Inc., Weingarten Realty Investors

(Image Source: Shutterstock)